Timothy Hawkins, superintendent of Kal-Tubing Company’s Machining Department, is very happy with his performance report for the past month. The report follows:

| KAL-TUBING COMPANY | ||||

| Overhead Performance Report – Machining Department | ||||

| Actual | Budget | Variance | ||

| Machine-hours | 22,500 | 26,250 | ||

| Variable manufacturing overhead: | ||||

| Indirect labour | 59,100 | 63,000 | 3,900 | F |

| Utilities | 152,400 | 178,500 | 26,100 | F |

| Supplies | 37,800 | 42,000 | 4,200 | F |

| Maintenance | 74,700 | 84,000 | 9,300 | F |

| Total variable manufacturing overhead | 324,000 | 367,500 | 43,500 | F |

| Fixed manufacturing overhead: | ||||

| Maintenance | 117,000 | 117,000 | 0 | |

| Supervision | 247,500 | 247,500 | 0 | |

| Depreciation | 180,000 | 180,000 | 0 | |

| Total fixed manufacturing overhead | 544,500 | 544,500 | 0 | |

| Total manufacturing overhead | 868,500 | 912,000 | 43,500 | F |

When he received a copy of this report, Wayne Lockhart, the production manager, commented, “I’ve been getting these reports for months now, and I still can’t see how they help me assess efficiency and cost control in that department. I agree that the budget for the month was 26,250 machine-hours, but that represents 8,750 units of product, since it should take three hours to produce one unit. The department produced only 5,250 units during the month, and took 22,500 machine-hours to do it. Why do all the variances turn up favourable?”

Required:

1. This part of the question is not part of your Connect assignment.

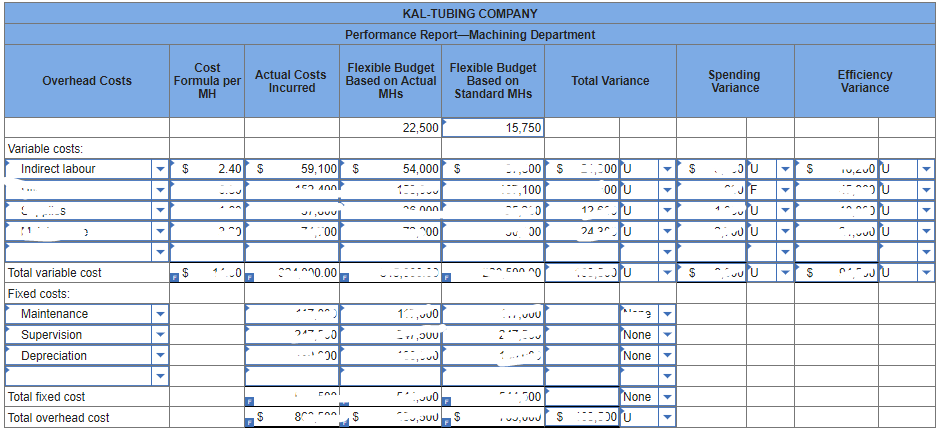

2. Prepare a new overhead performance report that will help Lockhart assess efficiency and cost control in the Machining Department. (Indicate the effect of each variance by selecting “F” for favorable, “U” for unfavorable, and “None” for no effect (i.e., zero variance). Round “Cost Formula per MH” answers to 2 decimal places.)

Related: (Solution) Koontz Company manufactures a number of products

Solution

Budgeted machine-hours 26,250

Actual machine-hours 22,500

Standard machine-hours allowed 15,750*

*5,250 units × 3 MHs per unit = 15,750 MHs allowed.

Please click on the Icon below to purchase the full 100% CORRECT ANSWER at only $3